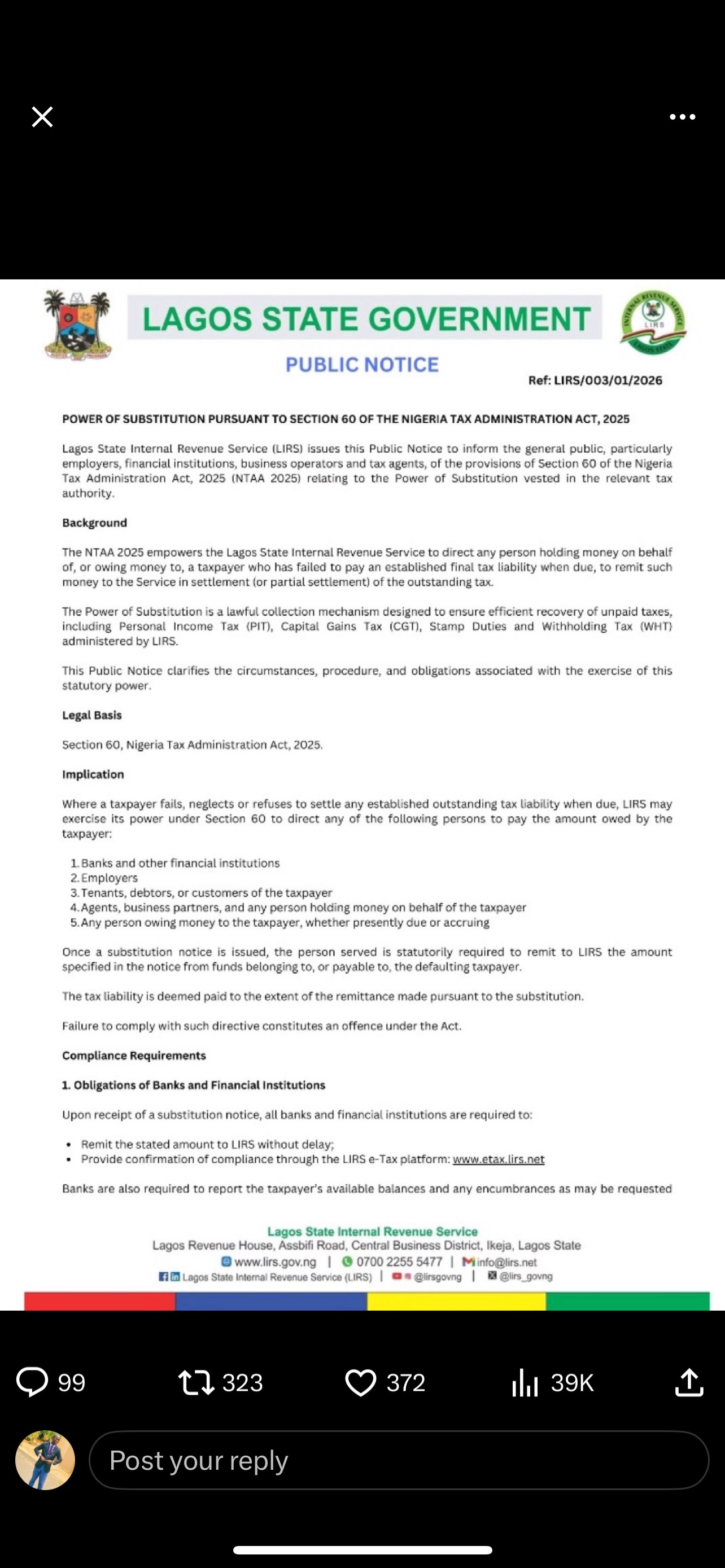

This is contained in a public notice issued by the Lagos State Internal Revenue Service (LIRS) on the “Power of Substitution pursuant to Section 60 of the Nigeria Tax Administration Act, 2025”.

The Lagos State Government has announced plans to begin seizing money belonging to defaulting taxpayers directly from their bank accounts and through third parties such as employers, tenants, debtors and business partners, as part of efforts to recover outstanding taxes.

This is contained in a public notice issued by the Lagos State Internal Revenue Service (LIRS) on the “Power of Substitution pursuant to Section 60 of the Nigeria Tax Administration Act, 2025”.

The notice was signed by the Executive Chairman of LIRS, Ayodele Subair, and dated January 21, 2026.

According to the notice, LIRS said it is informing “the general public, particularly employers, financial institutions, business operators and tax agents, of the provisions of Section 60 of the Nigeria Tax Administration Act, 2025 (NTAA 2025) relating to the Power of Substitution vested in the relevant tax authority.”

The agency explained that the law “empowers the Lagos State Internal Revenue Service to direct any person holding money on behalf of, or owing money to, a taxpayer who has failed to pay an established final tax liability when due, to remit such money to the Service in settlement (or partial settlement) of the outstanding tax.”

LIRS described the substitution power as “a lawful collection mechanism designed to ensure efficient recovery of unpaid taxes, including Personal Income Tax (PIT), Capital Gains Tax (CGT), Stamp Duties and Withholding Tax (WHT) administered by LIRS.”

The service warned that where a taxpayer “fails, neglects or refuses to settle any established outstanding tax liability when due,” it may invoke Section 60 to compel third parties to pay the debt on behalf of the defaulter.

Those who may be directed to remit such funds include “banks and other financial institutions,” “employers,” “tenants, debtors, or customers of the taxpayer,” “agents, business partners, and any person holding money on behalf of the taxpayer,” as well as “any person owing money to the taxpayer, whether presently due or accruing.”

LIRS stated that “once a substitution notice is issued, the person served is statutorily required to remit to LIRS the amount specified in the notice from funds belonging to, or payable to, the defaulting taxpayer,” adding that “the tax liability is deemed paid to the extent of the remittance made pursuant to the substitution.”

The agency further warned that “failure to comply with such a directive constitutes an offence under the Act.”

Specifically addressing banks and financial institutions, LIRS said that upon receipt of a substitution notice, they are required to “remit the stated amount to LIRS without delay” and “provide confirmation of compliance through the LIRS e-Tax platform.”

It added that banks are also required to “report the taxpayer’s available balances and any encumbrances as may be requested.”

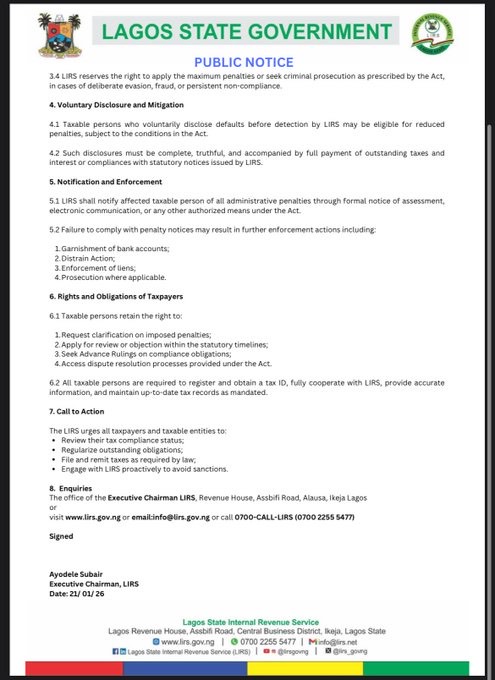

The revenue service also warned of stiff consequences for non-compliance, stating that it “reserves the right to apply the maximum penalties or seek criminal prosecution as prescribed by the Act, in cases of deliberate evasion, fraud, or persistent non-compliance.”

On enforcement, LIRS said it would notify affected taxpayers of penalties “through formal notice of assessment, electronic communication, or any other authorized means under the Act,” noting that failure to comply may result in actions including “garnishment of bank accounts,” “distrain action,” “enforcement of liens,” and “prosecution where applicable.”

While rolling out the enforcement framework, LIRS said taxpayers still retain the right to “request clarification on imposed penalties,” “apply for review or objection within the statutory timelines,” “seek Advance Rulings on compliance obligations,” and “access dispute resolution processes provided under the Act.”

The agency urged Lagos residents and businesses to “review their tax compliance status,” “regularize outstanding obligations,” “file and remit taxes as required by law,” and “engage with LIRS proactively to avoid sanctions.”